There's a number living in the back of most people's heads. A retirement finish line. $2 million. $3 million. Sometimes more.

Nobody calculated for them that the number was right. They absorbed it somehow, perhaps from a calculator, a colleague, a headline, or a commercial. And now the number is running their life. They're staying in jobs they're done with, deferring trips they want to take, and delaying retirement longer than they need to.

Here's what we find working with retirees and near-retirees in Minneapolis-St. Paul and remotely across the country: Most people need less than they think. And many could retire sooner than they think. The problem isn't the math. Most retirement planning overfocuses on longevity and worst-case scenarios, and completely ignores a more dynamic question: what if you never fully spent what you had?

There's another wrinkle worth naming early. Research cited in a 2024 Wall Street Journal piece found that retirees generally retire two to three years earlier than planned due to health, caretaking responsibilities, layoffs, or simply deciding they're done. Hal Hershfield, a psychologist at UCLA who studies the relationship between our present and future selves, noted that the gap between expectations and reality reflects how poorly we imagine the years ahead.

We expect the work to be available to us and for us to be able to complete it. That's often based on optimism about a future self who may not show up as expected.

We have worked with hundreds of retirees and see it regularly. At some point, people are just done with work, and the sentiment may set in quickly. The reasons run the gamut: burnout, boredom, shifting responsibilities, health issues, or bad leadership. The mentality shift can arrive quickly and unexpectedly. If they can retire securely on an earlier timetable, they want out.

Right now, you may assume you'll work well into your late sixties. That's understandable, and we absolutely support you if that is your goal. However, it also may be the wishful thinking of someone who hasn't yet seen how life evolves.

For what it is worth, most retirees are at least as happy as they expected to be once they get there. The question is whether they're financially ready when the moment arrives. In other words, do they have a written financial plan or not?

The Risk Nobody Talks About

Traditional retirement planning is obsessed with one risk: outliving your money. That's a real risk. It deserves attention. But in focusing on it so relentlessly, most planners ignore the mirror image of that problem: Underspending.

Underspending risk is the risk that you restrain yourself from spending on things that would bring you joy, out of fear that you'll run out of money later.

It shows up as skipped trips. Dinners you talked yourself out of. Help you didn't hire. Experiences you deferred until "later," forgetting to acknowledge that later may never arrive.

Most people assume the cautious path is the safe path. Often, it isn't. Holding back when you have the means and the health to enjoy your life is its own kind of loss, but it won’t show up in an online retirement calculator.

Before You Do the Math, Count What You Already Have

Here's a mistake that surprises me every time: people working through their retirement numbers often forget about Social Security entirely. They look at their portfolio, run the math, and conclude they don't have enough, without ever accounting for an income stream guaranteed by the federal government, adjusted for inflation every year, and impossible to outlive.

For a married couple in which both spouses work, combined Social Security benefits can easily run $50,000 to $80,000 or more annually. That income doesn't come from your portfolio. It doesn't shrink in a bear market. It doesn't require a withdrawal rate calculation. It just arrives.

For example, in 2022, stocks were down roughly 18%, and bonds fell approximately 13%, the worst year for both asset classes simultaneously in nearly 50 years, driven by the fastest pace of Fed rate hikes in decades. Yet Social Security proved a stalwart, increasing by 8.7% in 2023, the largest cost-of-living adjustment in over 40 years, and occurring precisely when retirees needed it most.

Timing when to file for Social Security matters enormously. For example, claiming at 62 versus 70 can change your lifetime benefit by hundreds of thousands of dollars. However, the point here is simpler: before you decide whether you have "enough" in your portfolio, you need to know what Social Security actually contributes to your income picture. Most people are pleasantly surprised.

If you're fortunate enough to have a pension or deferred compensation plan, the same logic applies. These income sources reduce the burden on your portfolio and fundamentally change the math behind your withdrawal rate. A pension covering $30,000 a year in basic expenses is worth roughly $750,000 in portfolio value at a 4% withdrawal rate. That's an incredibly meaningful boost to your retirement.

The practical implication is this: your retirement number isn't just about your portfolio. It's about the gap between what you want to spend and what guaranteed sources already cover. For most people, that gap is smaller than they assumed.

Why the 4% Rule Isn't the Last Word

Most retirees fall into what we would call the income paradigm. They plan to live off the yield from their portfolio -- bond interest, stock dividends -- without touching the principal. It may sound prudent. In practice, it tends to produce portfolios that are too conservative, too bond-heavy, and too vulnerable to the one risk that quietly destroys retirement plans: inflation.

There's a better framework, and it starts with understanding where the 4% rule actually came from.

In 1994, researcher Bill Bengen studied every 30-year market period in the 20th century and identified the worst one. His conclusion: even in that worst-case scenario, a retiree could withdraw 4% of their portfolio in year one, increase that amount by inflation each year, and never run out of money over a 30-year retirement. It was a landmark finding and a genuine gift to retirement planning.

But most people, including many financial advisors, act as though retirement research stopped there. It didn't.

In 2004, financial planner Jonathan Guyton published research that significantly updated our understanding of retirement income. His framework, often called the Guardrail Approach, replaces a rigid annual withdrawal with a dynamic one. Rather than taking the same inflation-adjusted amount every year regardless of what markets are doing, you build bands on either side of your target income. In strong markets, you can take a bit more. In poor markets, you pull back modestly.

That flexibility changes everything, because retirement is dynamic. Retirees make thousands of spending decisions every year. They naturally adjust when conditions shift. A plan that accounts for that adjustment can support a meaningfully higher starting withdrawal rate than one that assumes the worst-case scenario every single year.

Guyton's research found that for portfolios with at least 65% in equities, initial withdrawal rates of 5.2-5.6% are sustainable over 40 years at a 99% confidence level, and rise to 5.7-6.2% at a 95% confidence level.

The math on that is significant. Say you sold your business and netted $2 million after taxes, with Social Security covering your basic living expenses. How much can you safely take from that portfolio?

Using the 4% rule: $80,000 per year

Using Guyton's framework at 5.6%: $112,000 per year

That's $32,000 more annually. An extra $2,667 every month. Enough to travel more, keep the lake house, help your kids, or simply worry about money less. That's not a marginal difference; it's an entirely different retirement.

One honest caveat: an initial withdrawal rate above 5.5% requires consistent, professional monitoring to make sure spending stays within the guardrails as markets move. Using a guardrail approach to retirement income isn't a plan you can wing. But for someone working with a qualified fiduciary planner who understands these frameworks and the inherent tradeoffs and complexities, it opens up real possibilities.

Retirement Is Dynamic. Your Plan Should Be Too.

The guardrail approach also aligns with an important finding from research on how retirees actually spend, and it cuts against one of the most common assumptions in retirement planning.

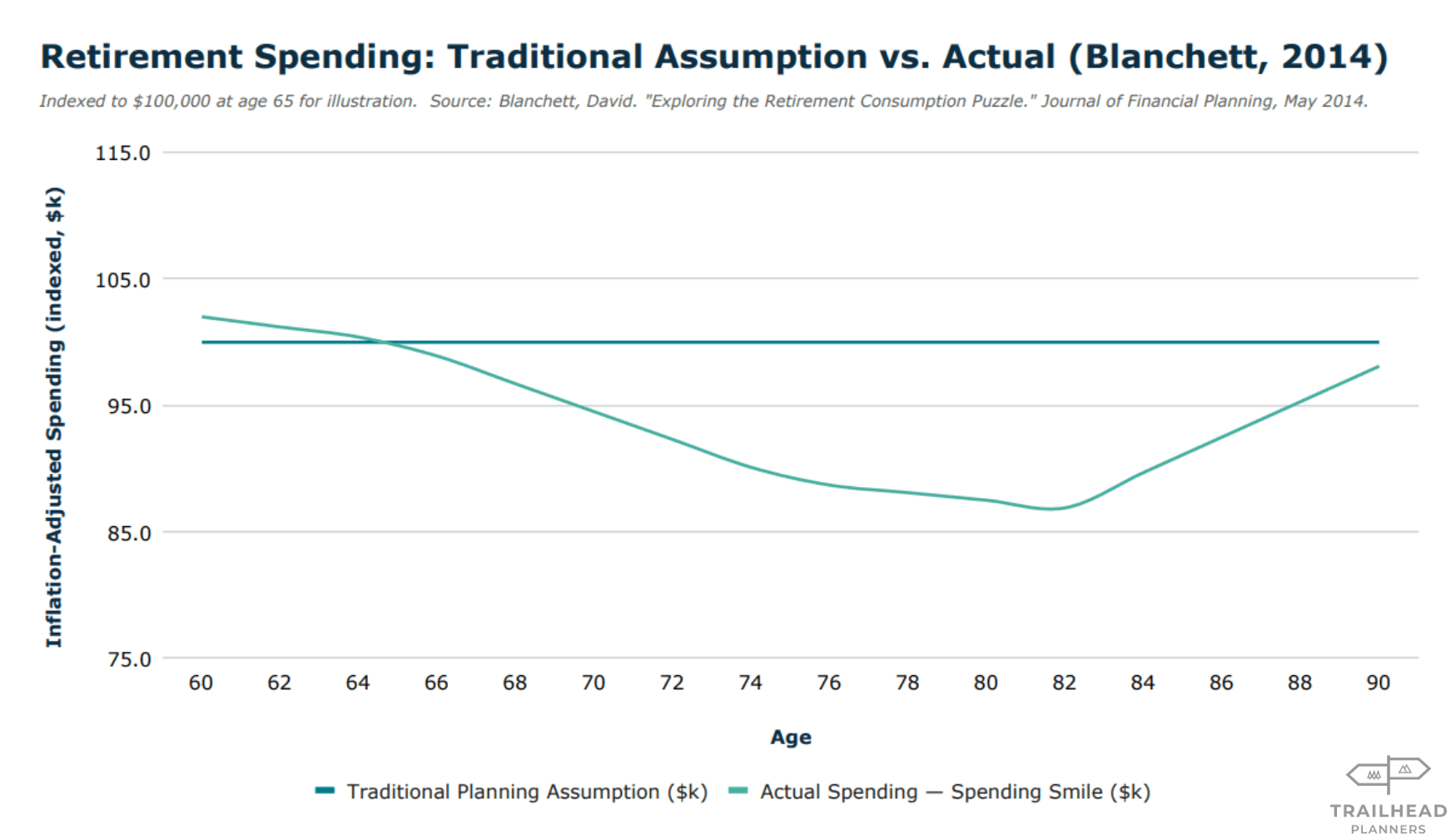

Most retirement tools assume your expenses increase with inflation every year, indefinitely. In a 2014 paper published in the Journal of Financial Planning, researcher David Blanchett analyzed actual retiree spending data and found the opposite. Inflation-adjusted spending tends to decline during retirement at roughly 1% per year on average. Blanchett traced the pattern of those changes and named it the "retirement spending smile."

Retirees tend to spend more in their 60s and early 70s. Maybe they enjoy travel, spending time with family, pursuing joy-filled activities or passions, or just staying active. However, inflation-adjusted spending then declines through the late 70s and into the 80s as activity naturally slows. Toward the end of life, it rises again as healthcare costs increase. Map out the spending patterns on a chart, and it looks like a smile.

This matters because most retirement planning fights this pattern rather than working with it. By anchoring to a conservative withdrawal rate and treating every year as identical, traditional planning restrains spending precisely when retirees most want to spend, and, conversely, leaves them flush in years when they may have less use for it.

Blanchett's data makes the underspending problem even more vivid. Among households with high net worth relative to their spending, actual consumption tended to increase from ages 65 to 75 before eventually declining. In other words, given financial security and good health, retirees naturally want to spend more in their early retirement years. The problem is that most retirement plans are built to prevent exactly that.

A dynamic plan matches the shape of a real retirement. More income when you can use it. Modest adjustments when conditions require. And a clear-eyed understanding of what "risk" actually means in this context.

Justin Fitzpatrick, the founder of Income Lab, a retirement cash flow software we have used at Trailhead Planners, frames it well: if retirees fail to achieve the income they hoped for, they don't run out of money. They don't experience financial ruin. They adjust, just as they would have during their working years. Retirement risk is better understood as the risk of adjustment, not the risk of failure.

Think about what that actually means. The main risk in retirement isn't running out of money. It's having to trim spending by ten or fifteen percent in a bad market year. For most of the retirees we work with, that's a familiar kind of uncertainty, far less daunting than what they navigated as they built their careers and engaged with questions around saving, investing, and spending over the decades.

What "Enough" Actually Means

At Trailhead, we think about this through a concept author Brian Portnoy calls Funded Contentment in his book The Geometry of Wealth: How to Shape a Life of Money and Meaning. The goal of your financial plan isn't to die with the most money. It's to have enough. Enough to live fully, give generously, and face whatever comes with confidence.

That means your retirement number isn't a single fixed figure. It's the intersection of what you want your life to look like, what a well-constructed dynamic plan can sustainably support, and what tradeoffs you're genuinely comfortable with.

For most people we work with, that number is lower than they assumed. And the retirement date can be closer than they had dared hope.

A Few Things Worth Thinking Through

If you're trying to get a clearer picture of your own retirement readiness, here's where we'd start:

What do you actually want to spend on? Not a budget. A life. Travel, grandkids, downsizing, a second home, philanthropic giving, time with friends. What does a good retirement actually look like for you, and what does that cost?

How comfortable are you with a dynamic plan? The guardrail approach and other dynamic approaches to retirement cash flow work, but they require accepting that your income may adjust modestly in bad markets. It is important to decide how much ‘risk of adjustment’ you can handle.

What's your tax situation? Thoughtful Roth conversion strategy, Social Security timing, asset location, and withdrawal sequencing can meaningfully increase the net income available to you throughout retirement. This thoughtful tax planning is often where the biggest gains are hiding.

What do you want to leave behind? Legacy goals and lifetime giving shape how much you need, when you need it, and how aggressively you can spend along the way.

The Bottom Line

Many retirees spend their final working years accumulating more than they need out of fear, then spend their early retirement years holding back out of the same fear.

The honest answer to "how much do I need to retire?" may be less than you think. You just need a financial plan built for how retirement actually works, not a worst-case scenario that treats every year the same.

If you're trying to get your arms around that number, we're happy to take a look. That's exactly the kind of conversation we have at Trailhead Planners.

Morgan Ranstrom, CFA, CFP®, CEPA®

Morgan Ranstrom is a CFA, CFP®, and CEPA® based in Minneapolis, Minnesota. He works with retirees and business owners across Oregon and Minnesota on tax-smart wealth strategies, including estate planning for families navigating Oregon's $1 million and Minnesota's $3m exemption thresholds. He is a fiduciary advisor, meaning he is legally required to act in your best interest.