The Big Mistake: Private Credit, Sexy Investments, and Why Boring Wins

Morgan Ranstrom, CFA, CFP®, CEPA®

When Blue Owl Capital made national news in early 2026 for halting redemptions from its private credit funds, many investors got a crash course in something their advisors never explained.

Investors in Blue Owl's $36 billion flagship fund had asked to pull out 21.9% of shares in a single quarter. The smaller tech-focused fund? 40.7% of investors wanted out. Blue Owl capped withdrawals at 5%. That is not getting your money out; it is being told to wait in line. (Source: Bloomberg)

But this post is not really about Blue Owl. Blue Owl is just the latest.

Why Everyone Was Rushing Into Private Credit

To understand how investors ended up here, you have to understand the appeal.

The Yield Was Genuinely Compelling

In a world where savings accounts were paying almost nothing and bond yields had been suppressed for years, private credit funds emerged, offering distributions of 10%, 12%, and sometimes 16% annualized. For high-net-worth investors who remembered the days when their portfolios threw off meaningful income, it felt like a return to something real. (Source: CNBC)

No one fabricated the potential yield. Direct lending to private businesses does generate meaningful returns because those businesses cannot access public bond markets and must pay a premium for capital.

However, that is exactly the problem. The yield is high because the risk is high.

It is called a risk premium, and the two (high yield and high risk) are inseparable. But in the pitch meetings and the portfolio reviews, the yield got the spotlight. The risk stayed in the footnotes.

The Allure of Private Markets

Alongside the yield story came something more seductive: the idea that private markets are inherently superior to public ones.

There is a version of this argument that has some merit. Private markets can offer a premium return for accepting illiquidity. Certain sophisticated institutional investors, with long-term horizons and professional staff, have used private credit and private equity effectively.

But there is a version of this story that seldom gets told: the experience of a $50 billion pension fund investing in private credit is fundamentally different from the experience of a high-net-worth individual doing the same. The pension fund negotiates directly with managers, pays institutional fee rates, has dedicated staff to conduct due diligence, and holds a diversified portfolio of dozens of funds built over decades. The retail investor gets a packaged product, pays retail fees, relies entirely on the advisor or manager to evaluate the underlying loans, and often holds a single fund. The asset class may be the same. The terms, the access, the leverage, and the outcome are not.

But the argument gets distorted in the retail wealth channel. "Private" starts to feel synonymous with "better." Investors assume that because something is harder to access, it must be worth accessing.

The honest question is not whether private markets can generate higher IRRs. They sometimes can. The real question is whether they generate higher risk-adjusted returns, net of fees and taxes, for the typical high-net-worth investor. That case is much harder to make.

And even if they do, there is a second question nobody asks: Is the illiquidity worth it?

Your money gets locked up for years. You cannot rebalance around it. You cannot access it when your business needs capital, you want to retire, buy a new house, a better opportunity arises, or life simply does not go according to plan. Liquidity has real value. Giving up liquidity should come at a meaningful premium. For most retail investors in private credit, it did not. Worse, few investors understand they are making the tradeoff in the first place.

The pitch might say you will get your money back in 5 or 7 years. That sounds manageable. What the pitch does not account for is that events change. 2020 hits. The Great Recession arrives. A credit crisis ripples through private markets. Suddenly, the five-year fund is in year ten, and distributions have yet to materialize. The timeline you agreed to and the timeline you actually experience are two different things, and the difference is not something you can negotiate your way out of once you are in.

In public markets, you have price transparency, liquidity, regulatory oversight, and a competitive market of buyers and sellers that does a reasonably good job of pricing risk. In private markets, valuations are often held at cost or marked up slowly. The portfolio looks less volatile on paper, but that is partly because the public market is not transparently pricing private funds and their holdings in real time.

This perceived lack of volatility is part of what is sold. However, in reality, the market price of the fund or the individual loans fluctuates; it’s just not reported daily like in public markets.

The volatility is still there. You just do not see it until you try to get your money out.

The Exclusivity Effect

There is also something more psychological at work.

Fund sponsors market private credit funds as exclusive. Not everyone could access them. You had to be an accredited investor. Your "private wealth advisor" at a big firm had a special relationship with the manager. You were getting access to something your neighbors could not get.

This feeling of exclusivity is a powerful feeling. It is also a dangerous one.

Exclusivity is not a return. Access is not an edge. The feeling of being a sophisticated investor is not the same as being one.

What They Did Not Tell You

The Tax Problem

Private credit income is taxed as ordinary income, not at capital gains rates. The top federal rate on ordinary income is 40.8%. The top rate on long-term capital gains is 23.8%.

That difference compounds badly over time. Bernstein Private Wealth Management ran the math: on a $5 million investment in private credit, assuming a 10% pretax return taxed entirely as ordinary income at the highest federal rates, the tax drag totals $4.3 million over ten years. (Source: NBC News)

"On a $5 million investment, the tax drag can total $4.3 million over ten years. That is not a rounding error. That is a second portfolio."

And that is before state taxes are factored in. Many of our clients live in Minnesota, Oregon, California, and other states with high income taxes. In Minnesota, the top marginal state income tax rate is 9.85%. A Minnesota investor in the top federal and state brackets is looking at a combined ordinary income rate approaching 50%. Investors in Oregon, California, and New York face similar or higher combined burdens. That 10% or 12% yield starts to look very different when half of it belongs to the government before you spend a dollar of it.

One individual we worked with had his former advisor incomprehensively put private credit inside his family’s irrevocable trust. Irrevocable trusts hit the top federal income tax bracket at roughly $15,000 of income. You could not design a worse structure for this asset if you tried.

As an aside, this is why tax location - placing particular investments and asset classes in the most tax-efficient account structure - is so important and valuable. Unfortunately, most investors, and even the vast majority of financial advisors, fail to take advantage of this opportunity. At Trailhead Planners, we incorporate focused tax location across all investment accounts for every household we serve.

The Fee Problem

Private credit managers typically charge both an annual management fee and a performance fee. Once you account for both, a 15% gross yield can deliver roughly 4% in your pocket, after taxes and fees. (Source: ArchBridge Family Office)

"The yield headline and the after-tax, after-fee reality are two entirely different numbers. Investors were sold the headline."

The Fine Print on the Distributions

Read the fund disclosures carefully. Blue Owl's own documents noted that distributions may be paid from sources other than cash flow from operations, including borrowings and return of capital.

In plain language: some portion of the "income" you were receiving may have been your own money coming back to you, dressed up as a return.

The Valuation Problem

One important fact failed to make the private credit pitch: you often do not know what your private credit investment is actually worth.

Without continuous mark-to-market requirements, private fund returns may not accurately reflect the true health of the underlying assets. The portfolio looks stable on paper because it is not repriced in real time. The risk is still there. You just cannot see it.

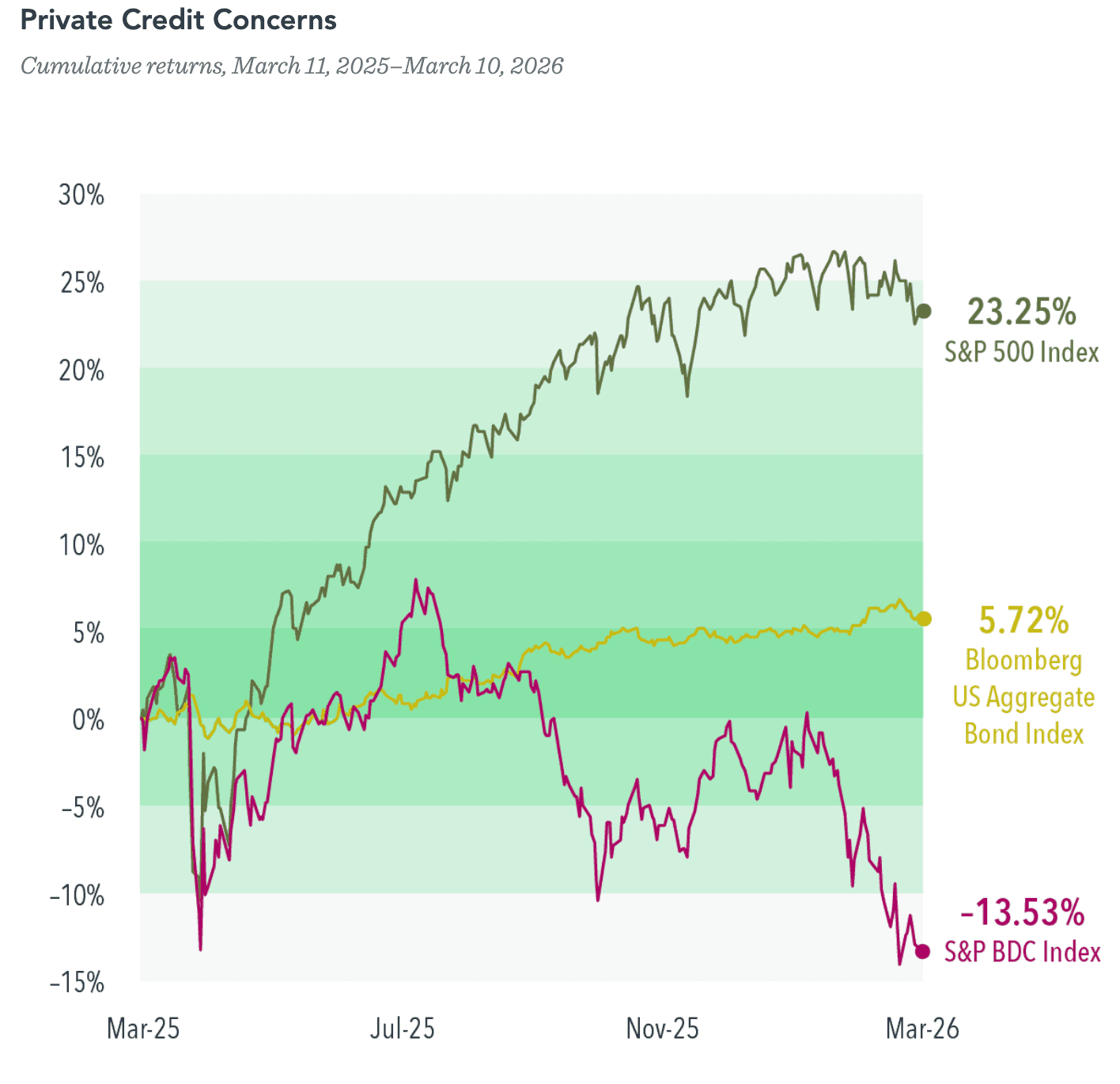

Dimensional Fund Advisors, one of the asset managers we work with at Trailhead, pointed to business development companies (BDCs) as a useful real-time signal. BDCs are publicly traded funds that hold primarily private credit debt. Because they trade on exchanges, they offer a continuously updated market view of what private credit assets are actually worth.

That view is not encouraging. While the broad US stock and bond markets have both risen since March 2025, an index of BDCs is down more than 13% over the same period. If BDCs are a reasonable proxy for what is sitting inside private credit funds, the market is telling you those assets are worth meaningfully less than they were a year ago. The private credit fund statements may not be reflecting that yet.

Source: Dimensional

The Liquidity Problem

Private credit funds are illiquid. When a fund lends to private businesses, it cannot sell those loans on an open market the way you can sell a Treasury bond or a stock. There is no ready market of buyers.

The lack of liquidity is a feature, not a bug. However, when everyone wants out at the same time, there is nothing to give them.

Which is exactly what happened with Blue Owl.

Not a New Story

Blue Owl is just the latest. Every generation has its version of the sexy, exclusive investment that turns out to be a lot more complicated than the pitch suggested. The names change. The story does not.

Junk bonds, 1980s. Michael Milken and Drexel Burnham made high-yield debt feel like an insider's game. Sophisticated investors who got access to the good stuff. Until the whole thing collapsed in fraud and defaults.

Tax shelter limited partnerships, 1980s. High-net-worth investors piled into complex LPs promising fat tax write-offs and income. The Tax Reform Act of 1986 changed the rules overnight. Many investors were left holding illiquid, worthless interests with no way out.

Emerging market debt, 1990s. Exotic yields from developing countries felt like a smart diversification play. It ended with the Russian default, the collapse of Long-Term Capital Management, and many very smart people explaining why they had not seen it coming.

Dot-com IPOs, late 1990s. Getting allocation in the hot IPO of the moment felt like being on the inside. The Nasdaq fell 78% from peak to trough. It took fifteen years to recover.

Structured products and CDOs, mid-2000s. Financial engineering turned pools of subprime mortgages into AAA-rated instruments that promised safe, steady yield. The complexity made the product feel sophisticated. It was the centerpiece of the Great Recession.

Hedge funds, 2000s. Two-and-twenty fees, minimum investments in the millions, and the sense that you had to be invited. The mystique around market-neutral strategies and uncorrelated returns faded as most funds underperformed a simple index fund after fees.

Non-traded REITs, 2000s-2010s. Illiquid real estate funds sold through the same advisor channel now pushing private credit. Salespeople promised higher yields, but high commissions were the underlying reality. When office real estate collapsed post-pandemic, many investors faced years of gated redemptions. Sound familiar?

Private equity, 2000s-present. The endowment model — Yale does it, so should you — made institutional-style private equity feel essential for any serious portfolio. The returns look great on paper. The fees, the illiquidity, and the question of whether returns survive rigorous risk adjustment look less great on closer inspection.

Crypto, 2020-2022. Decentralized, exclusive, and you either got it or you didn't. Bitcoin hit $69,000. Then it didn't.

SPACs, 2020-2021. Blank check companies that let retail investors get into pre-IPO deals alongside big names. The returns were almost universally terrible.

Private credit, now. High yields. Exclusive access. Sophisticated investors only. Redemptions gated. Tune in next time.

Investors like sexy. They always have. Every generation has a cohort of product salespeople ready to supply it. And every generation has a cohort of advisors who mistake complexity for quality and exclusivity for edge.

The pattern is not random, but a feature of how financial products get distributed and of human psychology.

New asset classes.

Compelling narrative.

Strong recent performance.

Urgency.

Exclusivity.

By the time the new hot investment gets pitched to retail investors through the private wealth channel, someone else has likely already captured the opportunity. Your buy-in is their exit liquidity.

What Actually Works

At Trailhead, our job is to protect clients from the big mistake.

Not just from any single bad investment, but from the pattern: chasing yield, chasing exclusivity, chasing the thing that feels exciting at exactly the moment when caution is most warranted.

The alternative is not complicated. It is just less exciting to talk about.

Get a solid financial plan in place. Set clear goals with real numbers and honest timelines. Know what you are trying to accomplish, and by when, and with how much risk you can actually tolerate, not just the risk you say you can tolerate in a good market.

Build an investment portfolio designed to achieve those goals. Not the portfolio that generates the most interesting conversation at dinner. Not the portfolio that signals sophistication. The portfolio is solid, diversified, and risk-conscious, with an expected return that is sufficient to meet your actual goals.

And then stick to it, with minor adjustments as your goals, markets, and life evolve. Rebalance. Stay the course. Do not let the next compelling narrative pull you off your path.

The effective advice is not the advice that fills a pitch book. It will not make you feel like a special investor. But it is the advice that actually works, and it is the advice that keeps you from sitting on a waiting list, wondering when you will get your money back.

Boring, when it comes to investing, is the goal. Boring means you are sleeping well. Boring means your plan is intact. Boring means you did not make the big mistake.

"Boring, when it comes to investing, is the goal. Boring means you are sleeping well. Boring means your plan is intact. Boring means you did not make the big mistake."

Trailhead Planners is a Minneapolis-based wealth advisory firm serving entrepreneurs, business owners, and legacy-focused families. If you want to talk through whether your current portfolio is built around your goals or around someone else's incentives, we would be glad to have that conversation.