The 5 Biggest Risks to Confront in Retirement

Retirement comes with a set of risks that are entirely new and unique to the stage of life. If building toward retirement is all about saving, retirement is all about cash flow. In the financial planning industry, we call this accumulation (i.e., saving for retirement and building your investment portfolio) and decumulation (i.e., spending down your portfolio in retirement).

Each stage of your financial life comes with its own set of complexities, and retirement or decumulation is no different. The complexities are immense and can feel overwhelming. That's why it's often a good idea to get a professional consultation on your retirement plan to ensure you are thinking through the risks and opportunities in a comprehensive manner.

We suggest working with a Certified Financial Planner professional who operates under a fee-only business model and acts as a true fiduciary. You can learn more about fee-only and fiduciary financial planning here.

That said, we've distilled what we believe to be the five core risks most retirees face in this post.

#1 Inflation Risk

Most Americans haven't given much thought to inflation over the past decade, as inflation has stayed historically low. However, the Coronavirus pandemic and shifting demand completely disrupted old patterns, and inflation has sprung up with a vengeance.

Whether inflation stays elevated or not, the topic has come back to the forefront of retirees' worries. Why does this matter?

Purchasing power.

When decumulating, it's important to focus not only on expenses in today's money but also on what your expenses might look like 30 years from now. Purchasing power is the inflation-adjusted value of your dollars.

For example, let's assume Sally needs an inflation-adjusted $4,000/month from her investment portfolio. At the below inflation rates, compounded over 30 years, the dollar amount she will need to maintain purchasing power is:

2% over 30 years: $7,245

4% over 30 years: $12,974

5% over 30 years: $17,288

As you can see, regardless of the inflation rate, it is hugely important that your retirement income strategy takes purchasing power into account. Even at 2% annual inflation, $4,000/month doesn't go very far and has lost nearly half of its purchasing power. At 5% inflation, a rate that would be historically above average over the time frame but still something to consider, the purchasing power of $4,000 drops by 77%.

All to say, your retirement plan must take inflation and purchasing power into account when designing your lifetime income strategy. As you can see above, just putting your money under the proverbial mattress would be disastrous for Sally's retirement.

#2 Market Risk

What's the best way to confront inflation risk? Well, it's likely to involve taking market risk, that is, investing in stocks and bonds.

Bonds generally have lower volatility (i.e., ups and downs) than stocks but more than cash. And historically, they have done a satisfactory job of keeping up with inflation. That is to say, bonds haven't historically grown purchasing power, but they have maintained it. Unfortunately, real, inflation-adjusted interest rates are significantly lower than inflation right now, meaning that the bond segment of your portfolio may not maintain purchasing power.

Stocks have higher volatility but higher expected returns than bonds. Depending on your risk capacity and risk needs, stocks should likely be a core allocation in your retirement portfolio. Moreover, equity allocations have historically done a great job of outpacing inflation over the long term.

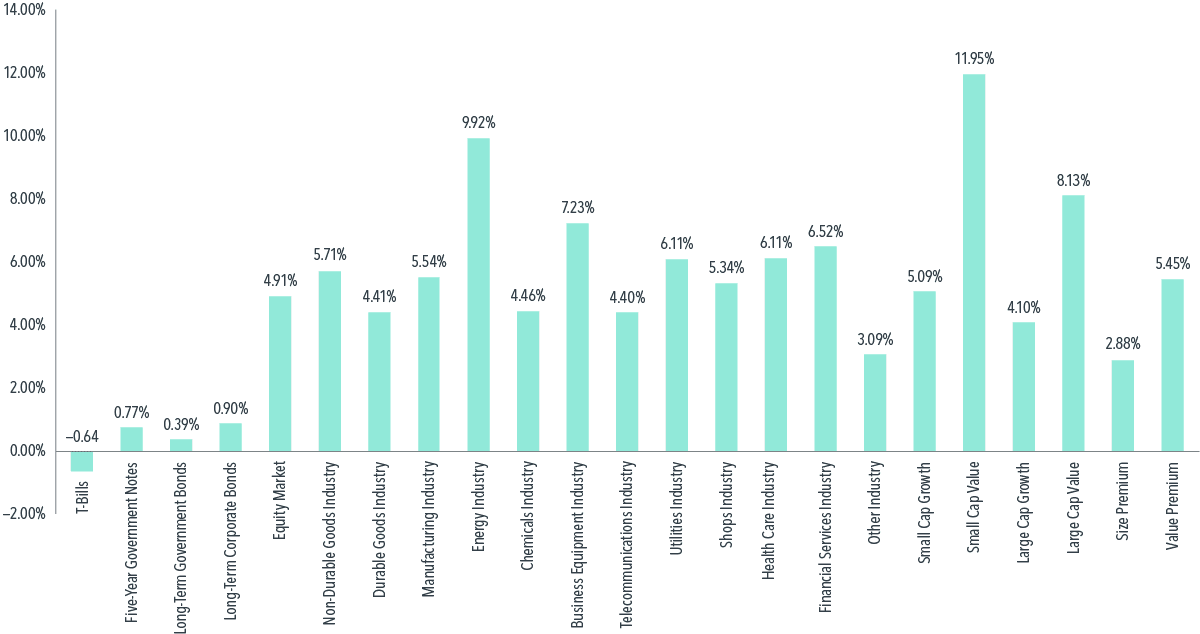

The chart below from Dimensional is titled "Keeping It Real: Average Annual Real Returns in Years with above-median US Inflation, 1927–2020." As you can see, stocks have generally performed just fine on average in periods of above-average inflation. More importantly, stocks have maintained, if not grown, purchasing power.

Source: Dimensional

#3 Behavioral Risk

Let's do a quick refresh. Because you want to maintain your purchasing power and overcome inflation risk, retirees end up taking 'market risk.' So, now that you're taking market risk, what's the risk?

Behavioral risk.

As you know, markets go up and down. This can be scary during your working years, but you have an income to fall back on. It can be downright paralyzing in retirement when you depend on your portfolio.

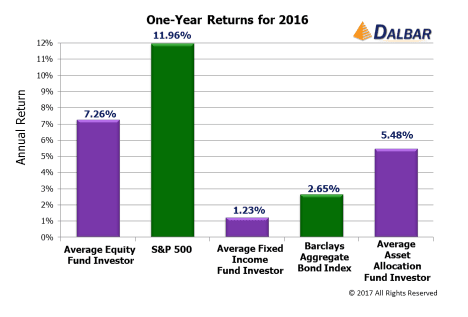

Behavioral risk is the risk that you don't end up sticking to your investment plan in retirement. Unfortunately, this happens quite regularly. DALBAR has worked to quantify what is often called the 'investor gap.' As you can see, in 2016, the average equity fund investor earned 7.26% while the overall index, the S&P 500 in this case, earned 11.96%. That 4.7% gap? That's the investor gap.

Source: Darbar's 23rd Annual Quantitative Analysis of Investor Behavior

Yet, volatility is the price you pay for the opportunity to earn stock market returns. To use an insurance analogy, volatility is the premium, while stock market returns are the payout.

Yet, no one really cares about volatility. They care about losing money.

That is, downside volatility.

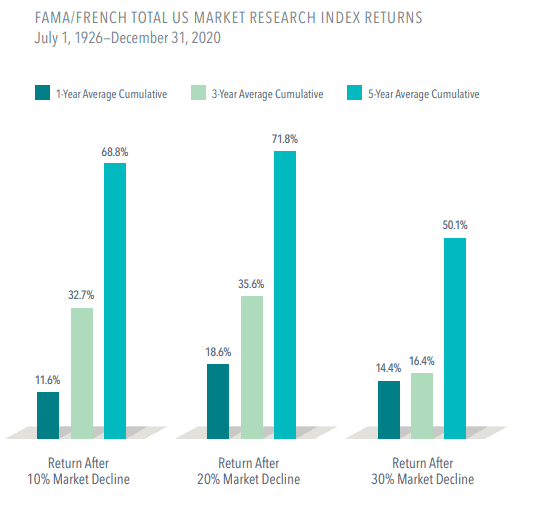

On this point, Dimensional put together the below great chart to show that market recoveries have historically followed market declines:

As you can see, the ensuing years after a market decline tend to contain positive market returns. In fact, they tend to be great years to be invested in stocks.

So don't succumb to behavioral risk.

Don't forget, it's 'buy low, sell high', not the other way around. By the way, hiring a financial advisor is a fantastic way to work toward overcoming behavioral risk. Who do you call when markets are down? Your panicking brother-in-law? Or do you call a calm, thoughtful, and experienced financial advisor who has guided clients through multiple bear markets before and who will help you strategically and patiently get to the other side?

#4 Longevity Risk

There are two options for retirement:

You can outlive your money.

Your money can outlive you.

There is no third option. And, by the way, most people prefer the first option. We suspect you are no different.

In the financial planning industry, longevity risk is the risk that a retiree outlives their money. From a health perspective, longevity risk is often perceived as good. You live a longer, and hopefully healthier, life! That's great. However, if your retirement funds were only supposed to last for, say, 25 years, and now they need to stretch to 35 years, that creates a risk.

Without getting overly complicated, there are a handful of ways to confront this risk:

Social Security: Social Security and other lifetime pensions last for the duration of your life. If you live longer than expected, they continue to pay out. Protecting against longevity risk also argues for deferring social security benefits for as long as possible to ensure the highest possible payout.

Annuities: Annuities may be an option to consider for a portion of your retirement funds to protect against longevity. For example, purchasing a longevity annuity can be an interesting option for many retirees to consider.

Withdrawal Rates: Managing your investment withdrawal rate for longevity risk is another option to consider. For example, you could lower your initial withdrawal rate, or you could plan on taking less inflation adjustments as the years go by.

All to say, confronting longevity risk is an important part of any retirement plan!

Bonus Section: What's the Opposite of Longevity Risk?

There is an oppositive risk to consider from longevity risk. We call this 'Underspending risk.'

Underspending risk is the risk that you will dramatically underspend during your retirement years compared to what you could have spent. Why is this bad? Well, as the saying goes, you can't take it with you.

And, of course, who doesn't want to take more trips, pay for more experiences, spend more money on their grandchildren, donate more to charity, or give more to their loved ones?

For this reason, it's a fine balance between longevity risk and underspending risk, but both must be confronted in your retirement plan!

#5 Long-Term Care Risk

Long-term risk is the final, highly important risk to confront in retirement. This is the risk that at some point during your retirement, you or your spouse may need a long-term care intervention. Generally, but not always, long-term care events happen toward the end of life.

Importantly, this period can last a couple of months, a year, or a number of years. According to Morningstar, over half of all individuals over age 65 will need long-term care at some point in their life.

Having a plan for long-term care costs, which can be quite high, is incredibly important to retirement security. Ultimately, there are three approaches to confronting long-term care:

Self-insure via your investment portfolio or another asset.

Buy long-term care insurance

Plan for Medicaid, which may require a Medicaid Spend Down Strategy

Conclusion

Though there are other important dynamics to any comprehensive retirement plan, we see these as the core risks:

Inflation Risk

Market Risk

Behavioral Risk

Longevity Risk (and Underspending Risk)

Long-Term Care Risk

Interested in creating a custom retirement plan to ensure you enjoy a tax-efficient, secure, and joyous retirement? Schedule a free introductory call with a Trailhead Planners Certified Financial Planner® professional below!

Morgan Ranstrom, CFA, CFP®, CEPA®

Morgan Ranstrom is a CFA, CFP®, and CEPA® based in Minneapolis, Minnesota. He works with retirees and business owners across Oregon and Minnesota on tax-smart wealth strategies, including estate planning for families navigating Oregon's $1 million and Minnesota's $3m exemption thresholds. He is a fiduciary advisor, meaning he is legally required to act in your best interest.